Invest in a Maverick

Quietly Building Rare Value

Picture a British entrepreneur, a maverick who has crafted a retail empire from humble beginnings. He stands among the UK’s most accomplished entrepreneurs, though the City often speaks his name with unease, bordering on disgust. His company, a vast retail powerhouse, moves to the rhythm of his unconventional strategies, having endured economic tempests, stirred controversy, and locked horns with the establishment, from media to government. While profitability fluctuates, the underlying figures reveal a calculated focus on long-term value creation, making this a stock that quietly but rapidly builds value while the market overlooks its potential.

This founder retains more than two-thirds of the shares, a clear testament to his unshakeable faith in his vision. Despite ESG missteps that have drawn scrutiny, the company’s knack for reinvention keeps it poised for growth, and it is currently repurchasing shares at attractive prices while channelling funds into transformative initiatives. With a valuation that appears undervalued yet ripe with opportunity, this stock beckons to those who can see beyond the noise. In this Deep Dive, we will explore why this stock is underappreciated for its maverick strategy for compounding shareholder value and, why it could prove an astute choice for patient investors seeking substantial returns.

In this Wonder Stocks Deep Dive, there are two documents. This is the short version, it includes the basic information to help investors gain an informed opinion on the opportunity. It is deliberately short and to the point. For those looking for more information, each section has a link to the Supplemental Article, which contains much more detail for those wishing to get into the nitty gritty. Any feedback, good or bad, about this style of article is greatly appreciated.

Wonder Stocks

Discover more wonderful investment ideas here.

Sportswear to Savile Row

In 1982, 18‑year‑old Mike Ashley borrowed £10,000 from his family and opened Mike’s Sports in Maidenhead, undercutting established rivals with rock‑bottom prices. Running the business as a sole trader until 1999, he refused corporate convention. When Sports Direct PLC listed in 2007, Ashley retained nearly two‑thirds of the shares. Over the next 18 years, the group made various acquisitions including Dunlop, Slazenger, House of Fraser, and Jack Wills which fuelled a book‑value that has risen by c. 16% per annum. Along the way, high‑profile missteps (the Shirebrook warehousing scandal) and boardroom skirmishes reinforced Ashley’s reputation as the City’s favourite pariah.

Yet these controversies mask a fundamental truth: underneath the combative headlines, Frasers has built operational excellence rivalled only by Next, with cutting‑edge warehouse automation and a scaled omnichannel platform. This friction between perception and reality is precisely what creates potential for outsized returns. Frasers Group has evolved far beyond its Sports Direct roots, emerging as a retail colossus with hundreds of stores across the UK, Europe and elsewhere, complemented by numerous e-commerce platforms.

For more information, click here.

Elevation

The Elevation Strategy has sought to reposition the company as a leading player in premium and luxury retail, moving beyond its discount sportswear roots. The strategy aims to enhance brand perception by forging deeper partnerships with high-profile names like Nike, Adidas, and The North Face, while expanding its premium lifestyle offerings through Flannels and acquisitions like Matches. It also prioritises an omnichannel approach, blending upgraded physical stores with robust digital platforms, and introduces innovative services like Frasers Plus to boost customer loyalty and drive sales. The overarching goal is to establish Frasers as the top sports and lifestyle retailer in Europe, the Middle East, and Africa, catering to a broader, more affluent customer base across diverse price points.

Frasers now operates over 750 stores across Europe, the Middle East, and Africa, plus multiple e‑commerce platforms. Its divisions include:

UK Sports Retail (Sports Direct): The original cash cow. It went through a period of difficulty around the exit of Dave Forsey but is now amongst the UK’s most profitable major retailer on operating margins challenging even Next’s.

Premium Retail (Flannels, Matches, Gieves & Hawkes): This is a core component of the strategy to target a wider range of price points and demographics. It is smaller than UK Sports Retail but is still a significant part of the business generating roughly 40% of the revenues of UK Sports Retail. It has grown largely through the acquisition of distressed assets trading at bargain prices.

International Retail: A growing footprint via stakes in Accent Group (Australia), Donnay (Belgium), and USC (Spain). As with the UK, international markets don’t have some grand strategy of empire building. Rather, it depends upon buying up assets as they become available at bargain prices and then integrating them into the Frasers platform. The international expansion strategy is similar to that of Premium retail.

Financial Services (Frasers Plus): Launched in 2023, offering buy‑now‑pay‑later and interest‑free credit, already servicing 377,000 active users and integrated with THG’s (formerly the The Hut Group) Ingenuity platform. Much like Next’s long-standing credit scheme, which has bolstered its customer retention by offering seamless payment flexibility tied to its retail and online platforms, Frasers Plus seeks to embed itself as a core component of the shopping experience, fostering stickiness and boosting basket sizes for a diverse consumer base. Like Next’s similar offering, it generates very high operating margins.

Complementing these is ELEVATE, Frasers’ retail‑media network (2025 launch), leveraging data from 30 million customers to monetise in‑store and digital ad placements. Together, these divisions form a diversified ecosystem few mainstream peers can replicate.

For more information, click here.

Credit Where it’s Due

Despite its track record, professional investors largely shun Frasers. Key objections include:

Volatile Earnings: Year‑to‑year profits have been inconsistent. Much of this occurred around the Shirebrook scandal and subsequent exit of Dave Forsey from the CEO role. That was nine years ago at time of writing and the company is on a much surer footing today.

ESG Shortcomings: Poor social and governance scores deter fiduciaries. The Environmental side comes about through the sale and third-party production of ‘fast fashion’ from abroad. Measures can and are being taken to address this. The Society part of ESG is largely a thing of the past. Whilst the reputational damage of Shirebrook remains, the group is in a much better position in 2025 than what it was in 2016. On the Governance side, it is inextricably linked to an investment in Frasers given the c. 73% ownership holding of Mike Ashley. ESG can sometimes be a rather blunt tool and individual investors have to make a decision as to whether they are comfortable with Ashley’s influence.

Combative Style: Public feuds with MPs, journalists, and former CEOs reinforce a negative image. The analyst community, most (all?) of which haven’t built any businesses let alone one employing more than 30,000 people, are quick to be dismissive of such achievements and can be rather flippant about questioning the company. This has led to times of fraying nerves from the management of Frasers. Combative communication is often the result.

Snobbery: There will always be a degree of snobbishness amongst UK professional investors on account of the predominance of pinky ring wearers. Ultimately, some of these people will never understand why Sports Direct and Frasers endures and prospers. They prefer steady-eddy well-spoken chief executives quietly, slowly but consistently going nowhere, to the cut and thrust of raw entrepreneurialism.

A pinky ring wearer who doesn’t work in the City

Yet every objection carries its counterpoint:

Volatility vs. Optionality: Frasers trades short‑term earnings consistency for reinvestment in asset acquisitions that compound capital. As Jeff Bezos wrote in 1997:

“When forced to choose between optimising GAAP and maximising future cash flows, we’ll take cash flows.”

Frasers follows a similar mantra.

ESG Evolution: Ongoing improvements in working conditions and governance, plus data‑driven retail media, indicate a gradual positive shift.

Combative Communications: Ashley’s forthrightness can be an asset as it deters complacency and signals alignment with shareholders through share buybacks.

Snobbery: Fund managers who embrace mavericks, who are often mavericks themselves, have quietly amassed outsized returns by backing Frasers.

For more information, click here.

Why It’s Cheap

At a market cap of c. £3.1 billion and whilst investments and net debt total to approximtely £500million, Frasers’ enterprise value sits at c. £2.6 billion using Wonder Stocks analysis, which adjusts for investments. Based on 2025 management guidance of £550-600 million Adjusted Profit Before Tax (APBT) and our estimate of £668 million underlying EBIT (see appendix), the business trades on c. 4x normalised EV/EBIT. For context:

Marks & Spencer: >10x EV/EBIT (two and half times as expensive as Frasers)

Next: >15x EV/EBIT (almost four times as expensive as Frasers)

Even if Frasers deserved only a Marks & Spencer multiple (10.7x), enterprise value would need to rise 175%, implying a market‑cap uplift of 147%. Given Frasers’ unique mix of deep value assets, superior margins, and shareholder‑friendly buybacks, a re‑rating seems overdue.

For more information, click here.

Management & Strategy: From Ashley to Murray

Ashley served as CEO until 2008, then stepped back to executive director. In May 2022, Michael Murray (his son‑in‑law) took the helm at 32, after modernising store formats and digital platforms in his previous role as Head of Elevation. Critics decry nepotism; supporters point to Murray’s rapid execution on Elevation initiatives. With Ashley retaining 73% of equity (as of October 2024, which is the most recent set of accounts) and ongoing consultancy, strategic continuity is assured. It should be remembered that a similar dynamic played out at Next, where Simon Wolfson faced nepotism claims upon becoming CEO in 2001 at age 33 while his father was chairman, only to prove his worth by elevating Next into a retail leader.

Under Murray, the Elevation Strategy has focused on:

Premiumisation: Deep partnerships with Nike, Adidas, and The North Face; targeted acquisitions of luxury labels.

Omnichannel Excellence: Upgraded flagship stores, a robust e‑commerce engine, and launch of Frasers Plus.

Retail Media: Monetising customer data via ELEVATE to boost third‑party ad revenue.

Operational Automation: Continued investment in warehouses and Customer Relationship Management (CRM) systems.

Early results are promising: footfall and online sales growth in elevated stores, pilot launches of ELEVATE generating incremental revenue, and Frasers Plus buy‑now‑pay‑later adoption are outpacing internal targets.

For more information, click here.

The Investment Case: Value + Growth = Upside

Value Proposition

Deeply Undervalued: c. 4x EV/EBIT vs. 10–15x peers.

Share Buybacks: Cancelling c. 5% of equity annually at cheap prices.

Asset Optionality: Property portfolio (Coventry Arena acquisition at £18 million vs. £113 million replacement cost) and stakes in listed companies enhancing hidden net asset value (NAV).

Value: Frasers looks very cheap.

Growth Proposition

Book‑Value Compounding: 16% compound average growth rate (CAGR) since 2007, which has tempered down to c. 10% in recent years. Even 10% CAGR over the next decade increases the book value by 160%, while 15% yields 305% growth.

Margin Expansion: As acquired businesses integrate, group margins should normalise upwards. This is hidden by additional acquisitions, which when value-accretive should continue to be made.

Retail Media & Financial Services: High-margin lines set to scale to £1 billion+ revenue (Frasers Plus) in the long term and multi‑million ad sales (ELEVATE).

Growth: Frasers is growing.

Combined Returns

Even the conservative case yields >20% p.a. over a decade; a profile rarely found in UK equities.

For more information, click here.

Risks & Mitigants

Share Consolidation Under Ashley: At current buyback rates, Ashley could approach 100% ownership in less than 10 years, which would mean that equity shareholders will be squeezed out. However, meaningful liquidity remains today, and board oversight continues.

Integration Overhang: One‑off costs distort short‑term profits; our EBIT‑based valuation strips these out. As long as the company is making regular acquisitions, which have been a rich source of value creation, then one-off costs will appear. Contrary to popular belief one-off costs associated with acquisitions should occur as it is evidence that a business is being properly integrated, with the elimination of duplicate processes.

For more information, click here.

Conclusion

Frasers Group is a textbook contrarian opportunity: a maverick founder, loathed by the establishment, operating a diversified retail‑finance ecosystem at a fraction of peer valuations. Share buybacks are boosting compounding, the Elevation initiatives are gaining traction, and the company’s assets offer real optionality. This is a stock for patient investors willing to embrace some controversy in pursuit of potentially transformational returns.

At its most bullish, an investment in Frasers over the next ten years could be truly outstanding, delivering over 1,000%. It may seem fanciful but Frasers is arguably extremely cheap with a long runway of double-digit growth. Truly exceptional returns, require truly exceptional vision.

For more information, click here.

Would you back a maverick with vision?

Disclaimer: the author of this Wonder Stocks article is Jamie Ward. At time of publishing he owns shares in Frasers Group

Appendix

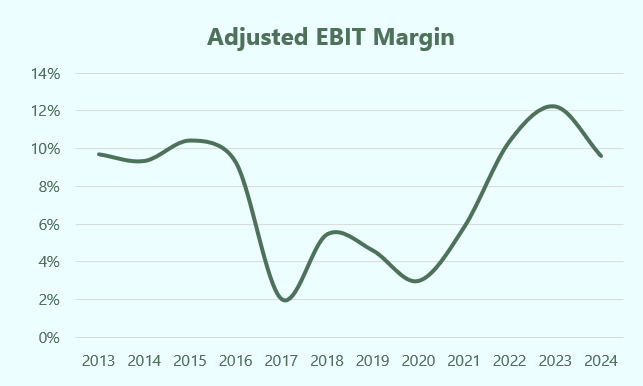

The chart below shows the four-to-five-year, starting in 2016, temporary decline in profit margins following the issues with the Shirebrook warehouse. The COVID-19 pandemic has obscured the picture somewhat, but the profit margin is now between 10% and 12% and closer to 15% at the UK Sports Retail business.

The chart below shows the path of free cash flow. Once again, the problems (starting in 2016) of the Shirebrook warehouse scandal are clear. In the years following, free cash flow was depressed as the group invested considerably more in improvements. Since 2020, free cash flow has returned to more normal levels given the profitability of the business.

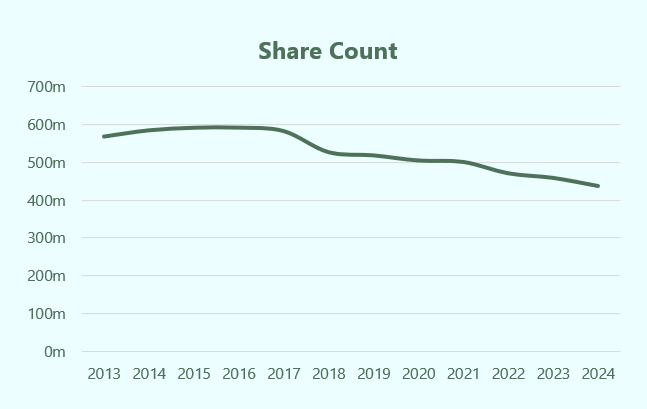

The chart below shows that the share count has begun declining as the group capitalises on its very low share price to boost per share value.

The chart below shows both earnings per share (green line) and adjusted earnings per share (yellow line) as well as consensus estimates from analysts.

How do you feel about MASH holding 73% of the shares. Is there a risk of delisting as extremely close to the 75% threshold.