Sometimes, the best investment opportunities emerge from temporary market dislocations rather than fundamental weaknesses. This UK-based small-cap company, a well-regarded brand in its sector, saw explosive demand during the COVID boom. However, as the world normalised, the business faced a period of destocking, leading to a sharp downturn in sales and a depressed share price. This overhang has masked the company’s true earning potential, but with inventory levels now stabilising and demand patterns normalising, the business is poised for a strong rebound. Investors willing to look beyond the recent turbulence may find themselves in a quality growth story at a deeply discounted valuation.

With a strong brand, loyal customer base, and improving market conditions, this stock has the potential to re-rate significantly as growth returns. Management has taken proactive steps to navigate the post-COVID challenges, ensuring that operational efficiencies and margins are set to improve. As revenue recovers and sentiment shifts, the stock could deliver between 350% and 500% in capital return alone. With limited analyst coverage and the stock still under the radar, now may be an opportune moment to get in before the market fully recognizes its turnaround potential.

Note: Wonder Stocks seeks to provide a narrative argument for its investment case. Nevertheless, supporting figures and charts can be found in the appendix.

Discover more wonderful investment ideas here.

Important Legal Disclaimer:

All "Wonder Stocks Deep Dives" represent the personal opinion of the author at the time of publication. These opinions may change over time without prior notice.

The author may or may not hold positions in the securities mentioned within these deep dives.

Please be aware that Wonder Stocks is not regulated by any UK authority. We make no guarantees regarding investment performance, and Wonder Stocks accepts no liability for any losses incurred as a result of acting on information presented here.

This blog is intended for sophisticated investors only. Wonder Stocks strongly recommends speaking to a qualified financial advisor before making any investment decisions.

For a full disclaimer, click here.

A Diamond in the Rough

Focusrite is a UK-based leader in audio technology company that was founded in 1985. It is a global business known for its high-quality audio interfaces and professional music equipment. Initially focused on high-end studio gear, the company broadened its reach over the years, catering to home recording enthusiasts, podcasters, and musicians at all levels. The company listed on the AIM market of the London Stock Exchange in 2014, providing it with the capital and strategic flexibility to accelerate its growth. Since then, Focusrite has pursued an expansion strategy, combining organic growth with a series of acquisitions to strengthen its market position and diversify its product offerings.

It operates several brands that cover a wide range of products but can be simplified into two broad categories; Production and Reproduction. Production is roughly three quarters of the business and refers to the process of creating, recording and manipulating sounds e.g., a musician in a music studio recording a new song. Reproduction, the final quarter of the business means the playback and delivery of sound to an audience, e.g., that same musician playing a concert at a venue.

Through a combination of internal development and acquisition, Focusrite has built up a suite of products that cater to the enthusiast market all the way to professionals. There is a considerable number of alternative products but Focusrite has a good and long reputation for producing well made, competitively-priced products and has generated considerable brand value.

A key pillar of Focusrite’s strategy as a listed company has been acquisitions, which have helped it diversify its revenue streams and strengthen its market position. It made its first acquisition in 2019 of ADAM Audio, a German manufacturer of professional studio monitors. The company followed this up with the acquisition of Martin Audio, a well-established name in live sound systems, further diversifying its business into the live music and events sector. Each of its acquisitions were made to help broaden the product offerings. In total, the company has spent c. £85m on six acquisitions in the last six years.

During the COVID-19 pandemic, Focusrite experienced an unprecedented surge in demand as lockdowns drove a boom in home recording, podcasting, and content creation. With musicians unable to perform live and many people exploring new creative hobbies, sales of audio interfaces, microphones, and studio monitors skyrocketed. This led to record revenues and profitability, as the company struggled to keep up with the surge in orders. The pandemic created a perfect storm of demand for Focusrite’s products, pushing its stock price significantly higher. However, as the world reopened, the demand spike inevitably faded. Many customers who had purchased recording equipment during the pandemic no longer needed to upgrade, leading to a post-COVID destocking period across the industry. Retailers and distributors, having overstocked during the boom, cut back on new orders, which hit Focusrite’s sales and led to a sharp correction in its share price.

An IPO Gem – 2014 to 2019

In the five years from its stock market listing to the beginning of the COVID-19 pandemic, Focusrite performed exceptionally well. Revenue, gross profit, net income, shareholders’ equity, dividends, and even net cash all rose significantly. The company rewarded its shareholders handsomely, with the stock price quadrupling over this period. All of this growth was achieved organically, but in 2019, the company made its first acquisition aimed at diversifying its business across the audio production and reproduction markets.

The acquisition of ADAM Audio was expensive, with Focusrite paying 18x earnings. However, at the time, Focusrite itself was trading on a PE of around 25x, making ADAM relatively cheaper by comparison. Shortly after, Focusrite acquired Martin Audio, a private equity-backed business making high-performance loudspeakers used in concerts. The timing was unfortunate, as Martin Audio is almost entirely reliant on live music and theatre. The acquisition was completed just three months before the first lockdown. Having paid around £35m for the business in December 2019, Focusrite wrote down its investment by more than £10m within nine months as demand collapsed.

A Share Price Rock Star – 2019 to 2021

Despite the initial struggles with Martin Audio, Focusrite’s core business saw enormous growth during the pandemic. With live music and theatre at a standstill, a surge in content creation drove unprecedented demand for audio production products. In the first year of the pandemic, Focusrite’s revenue rose 23% organically—a massive jump for a business accustomed to mid-single-digit growth. As lockdowns continued, this growth extended into 2021, with another year of 20%+ organic growth. Organic growth along with the acquisitions meant that revenues more than doubled, and net income nearly tripled. The share price surged, rising 200% in just 18 months to an all-time high of 1800p; a near 1200% return in less than eight years.

A Tarnished Gem – 2021 to Present

It’s easy to criticize the board for over-ordering during the demand surge, as excess inventory is a key issue today. However, during the pandemic, semiconductor shortages forced companies to secure as much supply as possible whenever it became available. Looking back from 2025, it’s clear the demand spike was temporary, but at the time, the board was navigating uncharted territory, making decisions based more on necessity than long-term strategy.

As is often the case, investors had extrapolated unsustainable trends into the future. The pandemic-fuelled surge in demand was unlikely to last and thus the very high share price was unsustainable. By the end of 2021, Focusrite had stocked up to meet demand, only to find that demand had sharply declined.

The result was a collapse in sales, shrinking operating margins, and a weakened balance sheet. Revenue declines led to fixed costs eating into profitability, while the shift from remote work back to normal business operations meant increased travel and trade show expenses. Inventory levels remained high, tying up capital in stock that customers were no longer clamouring to buy. As returns on capital declined sharply, Focusrite’s share price plummeted nearly 90% from its peak, wiping out all its pandemic-era gains—and then some.

Polishing the Gem – the Future

The company’s turnaround strategy is now well underway. Focusrite is in a destocking cycle, working to normalise inventory levels while positioning itself for future growth. Since the last pre-pandemic year in 2019, the company has completed six acquisitions, spending nearly £85m. It has invested £62m in internal development, largely for new product R&D, while also seeing working capital rise by £28m—a 150% increase from 2019 levels. Despite going through challenges, Focusrite has remained focused on innovation. The number of staff employed in product development has risen by 50% since the start of the pandemic. In the last twelve months alone, 35 new products have been launched. Even though it is going through difficulties, the company’s board is clearly still focused on the future.

During the pandemic, investors overestimated the long-term impact of a temporary surge. Now, they are making the opposite mistake, assuming the current struggles are permanent. History suggests otherwise. The last time business conditions were ‘normal’ in 2019, Focusrite shares traded around 600p. Today, despite it being a larger and more diversified company, the stock trades at a fraction of that value. If the company successfully normalises operations, an investment in Focusrite could be enormously profitable.

How Much Can Shareholders Make?

A return of 350% is suggested as the bullish case though one that doesn’t include outlandish assumptions. The timing of the return is uncertain and likely to be measured in several years therefore neither a return from dividends nor a compound average growth rate are provided. For reference however, at the time of writing, the dividend generates 3.5% and is forecast to rise c. 5% per annum hereon.

In order to generate the return, the following is assumed:

• Working capital returns to its old levels for the size of the business. This would imply a reduction of £9m, which would lead to a similar sized increase in the net cash position.

• Return on capital employed, taken as net operating profit after tax over capital employed (NOPAT ROCE), returns to the low end of its historic, pre-pandemic range. Historically, this measure ranged from 42% to 48.5%. A conservative 40% is assumed.

• Using the most recent trailing adjusted EBIT, the shares trade on an EV/EBIT of approximately 8x. During the pre-pandemic era, the shares traded in a range of 12.5x EV/EBIT to 23x EV/EBIT. Wonder Stocks conservatively estimates a return to the low valuation of 12.5x.

If working capital normalises, return on capital employed recovers to pre-pandemic levels, and the company returns to a low-end valuation of 12.5x EV/EBIT, a share price of 828p is achievable. This is still well below the all-time high but represents a significant upside. If returns and valuation move toward mid-range levels, the share price could exceed 1180p, delivering a 530% return before dividends. The market misjudged Focusrite at 1800p in 2021, and Wonder Stocks estimates it is misjudging it again today at 10% of that level.

In February 2025, the shares of Focusrite are valued on all time low levels of profitability combined with all time low valuation multiples. Should these normalise then big returns are on offer.

The main area that the company could disappoint is returning to old levels of return on capital employed. At time of writing, NOPAT ROCE (see Appendix) sits at around 17%; less than half of the average for the pre-pandemic years. It is feasible that the old levels of profitability are unattainable. Prior to 2024, the lowest recorded NOPAT ROCE was in 2018 at 42%. If we assume a conservative halving of this as a sustainable level together with a 12.5x EV/EBIT, the fair value drops to 432p, representing a capital return of 132%.

Final Point

The author of this Wonder Stocks piece is Jamie Ward. As at time of publishing, he does not own any shares in Focusrite. He is a fundamental analyst by training and presents the fundamental reasoning behind why he believes the shares offer good value. However, his purchases are made with the aid of technical analysis. He believes that the time to buy is very close.

Appendix

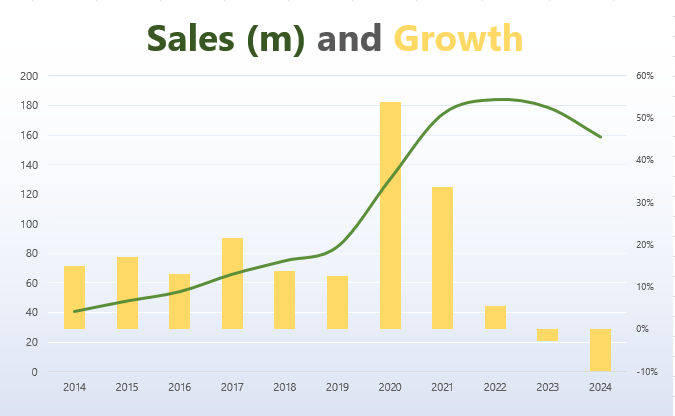

Sales Growth

In the ‘normal’ period before the pandemic, the sales rose by an average of 16% per annum. In the two years of the pandemic (2020 and 2021), the growth ballooned, averaging 44% per annum. Since then, the sales have declined with average growth rate for the most recent three years being -8%.

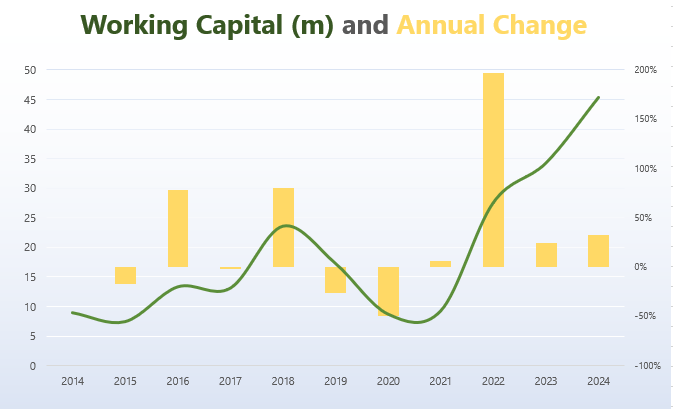

The Violent Swings in Working Capital

Having been relatively steady in the pre-pandemic era, the working capital collapsed as the company grappled with an unprecedented surge in demand. Since then, demand has fallen sharply but pandemic-era investments have now appeared on the balance sheet leading to extraordinarily high levels of working capital.

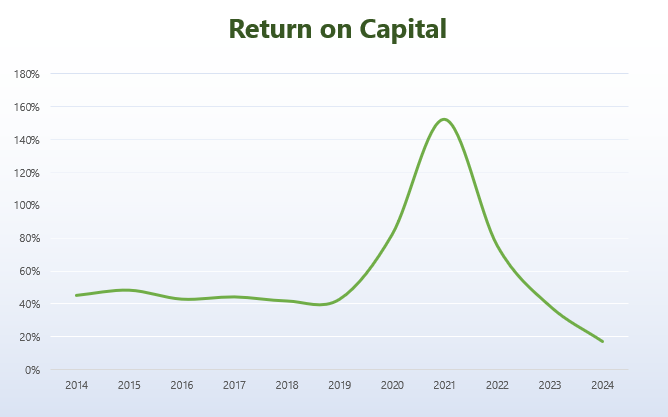

Return on Capital Employed

Having been fairly steady before the pandemic, return on capital exploded higher in 2020 and 2021. It has since declined to all-time lows. Investors were wrong to assume 2020 and 2021 were sustainable and paid a heavy price. Wonder Stocks believes that they are wrong too in 2025 to assume that the historically low levels are normal also.

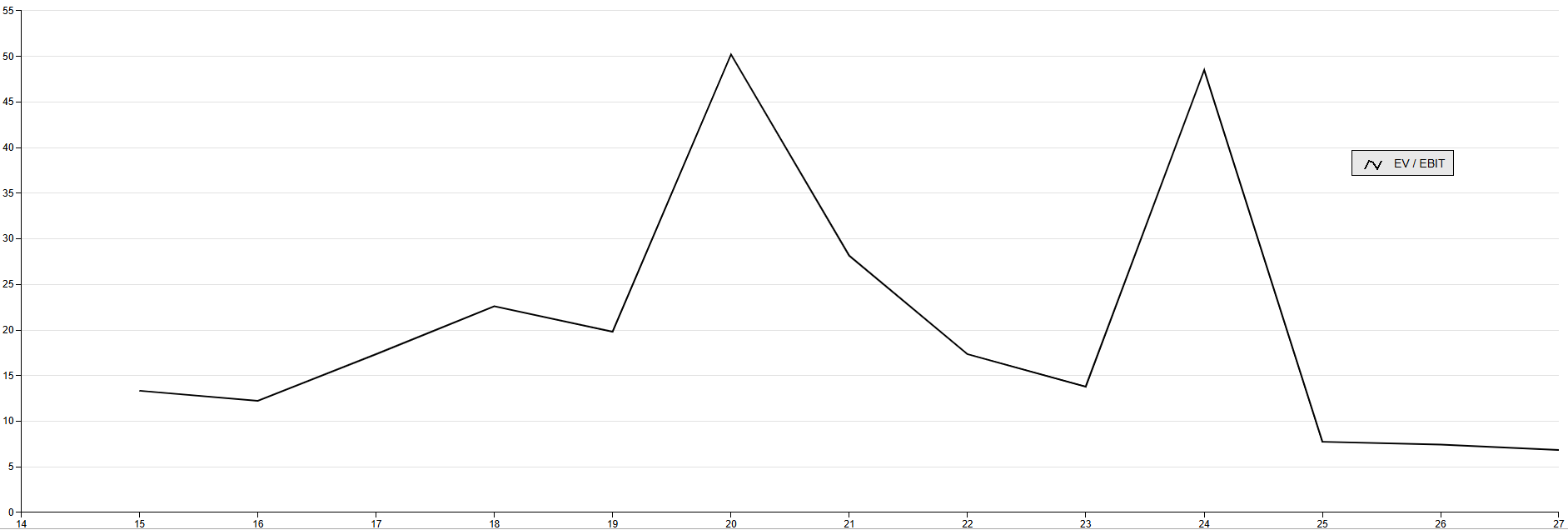

Historic Valuation

The EV/EBIT valuation for Focusrite is below (source ShareScope). For most of its existence, it has traded at a level between 12.5x and 23x. The valuation moved higher during the pandemic and currently shows as high because of heavy, one-off losses last year. Should the earnings and share price persist, the shares would trade on an EV/EBIT of around 7x by 2027.

Disclaimer:

The author of this Wonder Stocks piece is Jamie Ward. As at time of writing, he didnot own shares in Focusrite - bought bought on June 3rd of 2025. Unless stated otherwise, all sources of information come from Focusrite Report and Accounts, Focusrite presentations and Wonder Stocks’ analysis.

Yes, failing get to old levels of return on capital is the biggest risk and one that I identified. Remarkably, I can still make a case for a much higher share price even if returns on capital only return to half the the old lowest returns on capital. Margin of safety

Thanks for the comment

WS

Aka

Jamie

Excellent article. My favourite thing about your substacks is how industry focused they are. You really get a sense of the business and it's struggles / opportunities. How do you research this context so quickly and for so many companies?